How the Automobile Experience Will Change

Driver Experience: Everything we need in the context of our destination or driving there, like personalized destination search, real-time traffic and weather, location-based services, fuel consumption and payment will be molded into an experience that can easily be accessed while driving.

Driver Experience: Everything we need in the context of our destination or driving there, like personalized destination search, real-time traffic and weather, location-based services, fuel consumption and payment will be molded into an experience that can easily be accessed while driving.

Owner Experience: Vehicle connectivity will become a gateway to maintain better ownership relationships over the lifecycles of vehicles. More and more vehicles will self-diagnose problems and propose remedies like services visits, and to the extent of over-the-air software updates, will be practically “self-healing”.

Mobility Experience: Ultimately, connected cars will be just one of multiple means of transportation in the connected mobility value chain. By 2030, more than 70 percent of the global populations will life in megacities. In these dense urban environments, a connected vehicle will increasingly communicate with the transportation infrastructure and become part of the broader mobility ecosystem, including ride- and vehiclesharing and other modes of public transportation. This will require automakers to seamlessly integrate the personal vehicle experience with shared and public transportation options, since commuters will prefer a combination of modes to get from point A to point B in the most convenient, time and cost efficient way.

Smart Assistant: As a key hub in the web of the Internet of Everything, sensing what is happening in their surroundings, equipped with a portfolio of the rich experiences described above and learning our habits over time, the connected vehicle will eventually evolve to become a smart helper that can assist us with mastering some of our everyday chores. It will make proactive suggestions on how we can make best use of our time in transit, take us to our preferred destinations, where we like to eat or shop, notify us where friends are currently located, take us there using the least congested and safest roads, guide us to parking spots close by and even pay for parking and refueling.

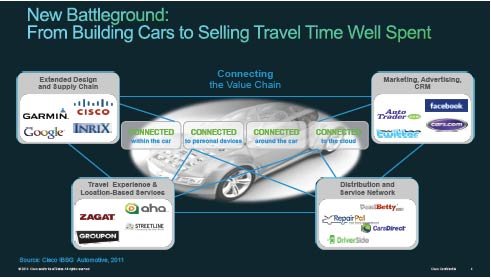

Five Critical Building Blocks

The value proposition of this new breed of personal mobility business will evolve around five major layers with a number of critical building blocks..

The value proposition of this new breed of personal mobility business will evolve around five major layers with a number of critical building blocks..

[box type=”shadow” ]Borrowing from Adam Smith, The Internet of Everything is “the dynamic engine of economic progress” of the 21st century. It boosts the benefits of “the division of labor” by the fusion of cyber physical systems and by sharing of costs and assets. As such, it is set to spawn a new profitable personal mobility business that has the potential to create $700 billion benefits for all of us around the globe.[/box]

First, the vehicle needs to be upgraded to make full use of its ability to connect to the outside world and to make it part of our everyday life. The starting point is a new operating and infotainment system with a user interface that is highly intuitive and allows operation with minimal distraction, and paired with personalization. Vehicle and user analytics will become key value creators for the “experience manufacturers” and feed the artificial intelligence engine that delivers contextual personalized experiences to drivers and owners. The integration with home security and automation and wearable health devices that monitor driver fitness will complete this innovation layer.

Innovation layer two integrates the vehicle with our virtual life, with the primary commercial goal of finding and getting people to virtual businesses. This includes the integration with social media, Internet search and electronic shopping and payment. The highest value for the business lies in big data analytics and the marketplace, where vehicle and user data is sold for value.

The next innovation layer perfects the capabilities of vehicles to easily find and efficiently direct people to real places. Intuitive destination and point of interest search, highly accurate maps and location, real-time navigation with traffic, weather and road risk, contextual location based services and electronic payment and guidance as to how to drive safer and more economically add value to this innovation layer.

Innovations on layer four physically gets people to real places, by integrating the vehicle into the multi-modal world of transportation with a multi-modal travel planner, including car- and ride-sharing options and mobility on demand (e.g., MyTaxi, Uber). Ultimately, autonomous vehicles will accelerate the convergence between personal and shared or public transportation and make it a viable alternative to vehicle ownership, especially for people who live in or close by large cities. The ability of businesses to pay for your trip to their branches are likely to make the lures of mobility on demand over vehicle ownership even more compelling.

The last layer of innovation integrates the value proposition with the infrastructure the vehicle uses. Pervasive network access with Wi-Fi along roads will be a differentiator in a world where all things connected congest our airwaves even more than our roads. Making it easy for people to find connected parking spaces is becoming a must-have in today’s new vehicles. Vehicles that connect to traffic lights will benefit from “eternal green light zones” and drivers will have perfect visibility at night when light intensity is calibrated between vehicle beams and smart streetlights (and save cities 30 to 50 percent in energy costs). “Hiring” a vehicle together with a dedicated lane or road in highly congested cities will be a highly attractive value proposition. With inductive charging maturing, the ability to recharge electric vehicles while driving on dedicated lanes would add more value, and also allow a reduction in the size and cost of vehicle batteries..

The Valley’s Role

The innovation leaders for most of the critical building blocks are located in “The Valley.” The additional challenge to the automotive industry and their traditional suppliers is that a number of these services are offered via “freemium” business models that are eroding business values of incumbents and creating barriers for new entrants.

The innovation leaders for most of the critical building blocks are located in “The Valley.” The additional challenge to the automotive industry and their traditional suppliers is that a number of these services are offered via “freemium” business models that are eroding business values of incumbents and creating barriers for new entrants.

“The Valley” can effectively transport three proven virtual business models into the physical world of personal transportation, which is a natural evolution of revolutionary business models.

With the value of the core product “vehicle” eroding and virtual mobility services and business models commanding a growing share of the value-add, automakers will increasingly be forced to expand their value proposition beyond the confines of the car and connect their vehicles with critical elements of the virtual mobility value chain.

Draining the Lakes?

“The Lakes” are facing a revolution of their evolutionary business model that has worked well for them for the past 100 years. Personal vehicle demand is increasingly cannibalized by a sharing economy and attractive intermodal offerings in mega cities, subsidized by B2B business models, all of which entices customers to give up personal vehicles ownership.

But the expanded mobility value chain, the virtual business models and the enabling technologies are outside of automaker’s core competences. So the industry debate is in full swing as to where the automakers can beat “The Valley” and where it would be of mutual benefit to join forces.

As some of the innovation leaders have “skin in the game” in the connected personal mobility value chain and are of equal or larger size than automakers, a traditional supplier-buyer relationship will likely be insufficient. Winners will work closely with nontraditional partners, will embrace different innovation models and will explore new business models.

The second major battlefield is the autonomous vehicle. Closing the technology gap to enable fully autonomous vehicles is confronting the automotive industry with very similar challenges, since many mission critical technologies are from innovation leaders outside of the traditional automotive supply base.

A key question to be resolved is which technology domains are an axis for competition as opposed to where standards or cost sharing or intellectual property would create crossindustry benefits. An innovation model that has worked very well for Cisco, distinguishes four different strategies that are applied on a spectrum from core to context.

Build, Buy, Partner or Collaborate?

New technologies that are regarded core and where proprietary differentiation is necessary would need to be “Built” or internally developed. To enter new markets or enhance existing ones, a “Buy” or acquisition strategy, potentially in collaboration with industrial or venture partners, is more appropriate. To bring new solutions to new markets, a joint go-tomarket “Partner” model is preferred. To test or spawn innovation and nextgeneration products and services in non-core domains to “Collaborate” with B2B customers or suppliers is a smart option.

For all mobility value chain partners, it boils down to what technology or cost elements of the value creation process can be controlled in the long run or should be shared for mutual advantage. Similarly, where does controlling or sharing access to customers or data turn into a sustainable single or mutual advantage for delivering value and differentiation?

Putting Together the Winning Team

As in a real race, it is less a question of building the fastest and sleekest car (“The Lakes”) or the coolest connected device to capture virtual value (“The Valley”) than who will put together the winning team across industries to deliver the superior experiences that become possible when cars connect to the Internet of Everything (IoE). For the partners in the future personal mobility value chain it will be critical to assess each one’s how the IoE will transform their business, what the winning IoE strategy will be, what partners they need to succeed and what IT investments they need to execute their IoE strategy.